MARCH 2025

2025 jobs were revised down by over 800,000

Non-farm payrolls have been revised down in 24 out of 25 months.

Source: Bureau of Labor Statistics

Monthly Revisions

February 2025

Loan Maturities

Refinancing risk for multifamily and commercial real estate debt will remain high for at least the next two years as much of the $957 billion in loans—including $310 billion in multifamily debt—that matured in 2025 received extensions

The Kaplan Group, which ranks among the top commercial collection agencies in the nation, has stated that the current multifamily maturity wall is fundamentally different from previous CRE debt crises in both scale and structural dynamics because it is a direct result result of the extraordinary acquisition activity in 2020-2022 when multifamily was seen as a pandemic-resilient asset class

Of the total $957 billion in CRE loans maturing in 2025, The Kaplan Group estimated only 50 to 55 percent were paid off

CRE Loan Maturity wall

$957 Bn

$539 Bn

$350 Bn

$550 Bn

January 2025

jay parsons’ observations from nmhc annual meeting

The NMHC Annual Meeting is the premier and largest gathering for the multifamily industry, held in Las Vegas bringing together over 8,000+ owners, developers, and investors for networking, market insights, and strategy

Jay Parsons is a rental housing economist, advisor and speaker. He has advised numerous multifamily and single-family rental housing stakeholders – from institutional investors, REITs, regional operators, lenders, regulators and government agencies. Jay hosts a weekly podcast called The Rent Roll with Jay Parsons, which in 2025 ranked among Spotify’s top 1% for most shared shows and in the 2% for listening time and for growth. Additionally, the readers of CRE Daily ranked The Rent Roll as the No. 1 housing podcast and No. 3 in all commercial real estate. In addition to independent speaking engagements and consulting, Jay serves as an Economics Advisor to JPI and a Strategy Advisor to Madera Residential. Previously, Jay was the Chief Economist at RealPage.

“Debt is abundantly available and at increasingly attractive terms – and that is having real implications. Debt funds are very eager to deploy capital and seem to recognize they’re not going to get the juicy terms they expected when those funds were raised. Borrowers thrilled. Higher-quality assets are recapitalizing with attractive terms and generous valuations (baking in future growth?), limiting the pain for sponsors and allowing them to wait out better times to exit. Abundance of debt = abundance of recaps = limited sales transactions. Mindset remains: Why sell now at a discount unless you have to?”

“Buyers (equity capital) remain very patient. Nearly everyone with equity is still targeting well-located newer-vintage assets – or maybe stretching to older vintages if in strong submarkets. That’s a very liquid market with some deals transacting in the 4s again, but it’s also a very thin market in terms of deal volume. More buyers than sellers (thanks to recap activity). For some would-be buyers with dry powder to deploy, I don’t know that reality has sunk in that (barring an epic collapse) they’re not gonna buy a lot of high-quality assets for quarters on the dollar. The problem is they’ve raised capital on the premise such deals would be widely available at huge discounts to replacement cost. But by now it should be obvious that most of those types of deals with maturing loans are recapitalizing rather than selling due to the abundance of available debt.”

January 2025

Unlike the other sectors in Tampa, multifamily recorded a 20% decline in sales volume year over year [from 2024 to 2025]. Overall, the market recorded $1.7 billion in total sales volume, which is also 33% below the annual average from 2015 to 2019. As vacancy rates have risen to a 15-year high and asking rents have declined for the better part of two years, investment sentiment has become more cautious. Large transactions, exceeding $100 million, which were a staple of transaction activity at the peak of the market between 2021 and 2022, were few and far between in 2025, with only four such transactions reported. Furthermore, only 40 transactions exceeding $5 million were recorded in 2025, compared to 128 transactions in 2021, when deal activity reached its peak.

Source: Costar

October 2024

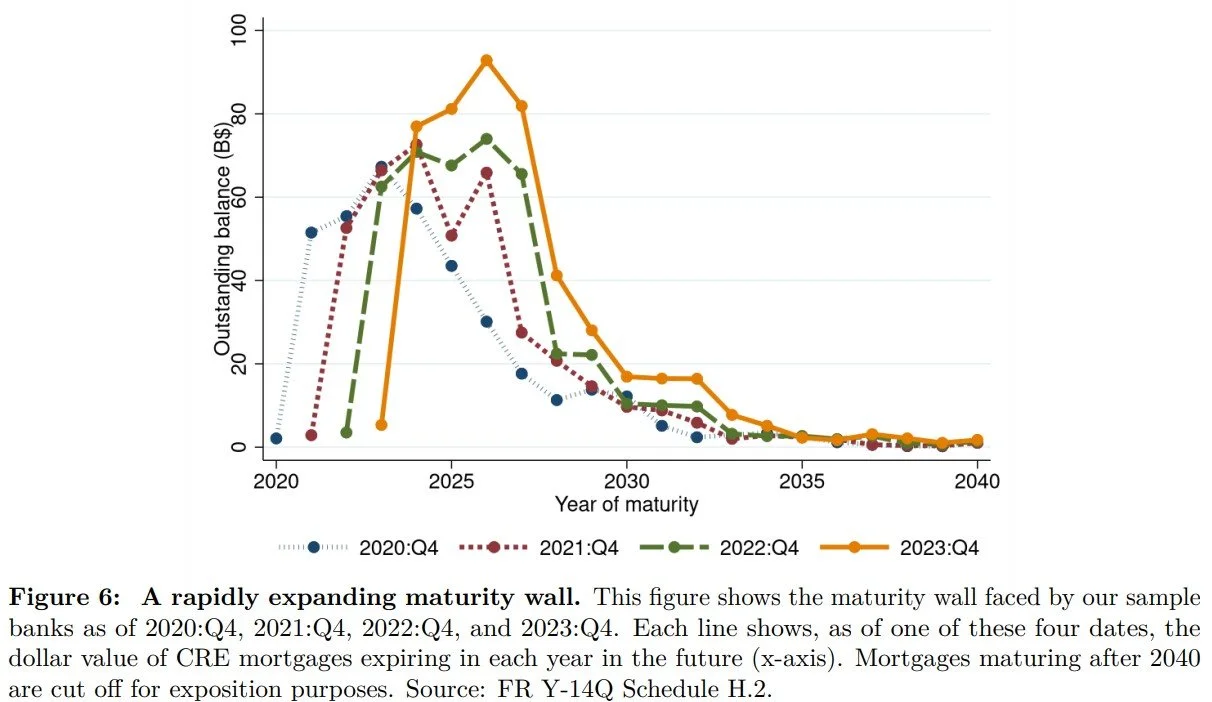

“We show that banks “extended-and-pretended” their impaired CRE mortgages in the post-pandemic period to avoid writing off their capital, leading to credit misallocation and a buildup of financial fragility. We detect this behavior using loan-level supervisory data on maturity extensions, bank assessment of credit risk, and realized defaults for loans to property owners and REITs. Extend-and-pretend crowds out new credit provision, leading to a 4.8–5.3 percent drop in CRE mortgage origination since 2022:Q1 and fuels the amount of CRE mortgages maturing in the near term. As of 2023:Q4, this “maturity wall” represents 27 percent of bank capital.”

Source: New York Fed https://www.newyorkfed.org/research/staff_reports/sr1130.html